Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 16.2.2022 at 16:09pm CEST

The current prices on the European carbon market are as follows:

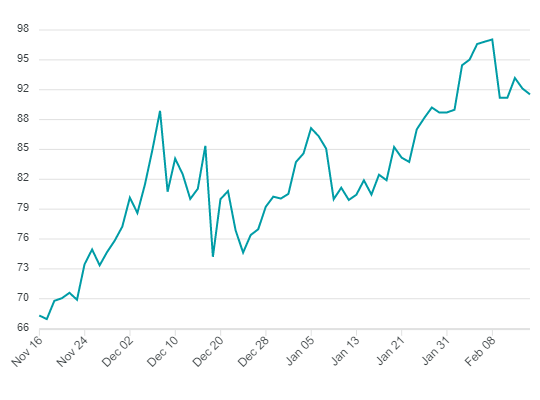

In the past week EUAs remained mostly range-bound, with no clear direction and mixed fundamentals. Uncertainty of what is going to happen on Russia-Ukrainian border seems to be subsiding, as Russian President Vladimir Putin was quoted for saying that he would favour a diplomatic solution. The main drivers of current price action remain weather and expectations of potential regulatory intervention. Political aim has been to introduce a solution that would not put a cap on EUA prices, but to prevent them from rising too fast. The news of MEP efforts to relax price control mechanism, and subsequently releasing 100 million allowances from Market Stability Reserve in the next six months, has hit the market in the morning hours. This has caused increased volatility and sharp selling activity as EUAs plunged by more than 3 EUR in only 40 minutes. However, market has rejected lower prices and rebounded higher, erasing the losses. Even though today market sold off rapidly, the suggested mechanism needs to be approved by three EU institutions: the Parliament, EU Commission and Council. It is estimated it would take more than six months to put in place potential new legislation. Auctions in the past week cleared mostly below secondary market, with lower cover ratios, which was usually a sign of short-term weakness in the market.

German power prices are down by 1.25 EUR since last week, with the front year contract trading at 136.75 EUR/MWh. API2 coal prices are down by 6.50 USD since last week, with the Cal23 contract trading at 110.50 USD/tonne. EUR/USD is down by 70 points since last week and is currently trading at 1.1360.

Price development of EUA Dec2022 futures contract