Pridobite najnovejše informacije iz trga emisijskih kuponov in se prijavite na brezplačno tedensko prejemanje novic

This newsletter was published 2.7.2025 at 16:54pm CEST

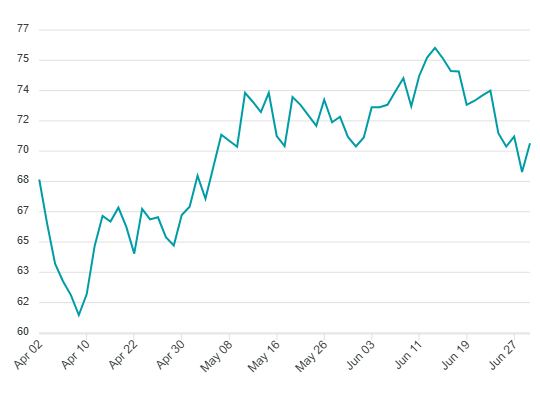

The current prices on the European carbon market are as follows:

July started on a very positive note following a period of strong selling activity that persisted until the end of June. This selling pressure may have been linked to options expiration as well as quarterly portfolio rebalancing. Once the selling subsided, the market staged a strong rebound, forming a V-shaped recovery. Importantly, this recovery was not solely driven by technical price action but was also supported by fundamentals. One of the most significant drivers was the heatwave that struck Europe last week and is still ongoing. This extreme weather has had notable effects on energy markets, particularly in the power sector. Unusually high temperatures typically increase energy demand, which is not only essential for residential cooling but also for industrial processes and power generation. In France, utility company EDF reportedly had to shut down some nuclear power capacity because river temperatures were too high. The heatwave has been compounded by a lack of precipitation, further contributing to the rally in energy prices. Lower water levels have negatively impacted hydroelectric power generation, adding to supply constraints. Additionally, the latest CoT report indicated a substantial reduction in investment fund positions, both long and short. Net long exposure fell by nearly 8 million tonnes week-on-week, totalling approximately 15.6 million allowances as of Friday’s close. Whether these factors alone are sufficient to sustain the upward momentum is yet to be seen; however, fundamentals have not been this favourable for the bulls in quite some time.

German power prices are down by 0.94 EUR since last week, with the front-year contract trading at 86.50 EUR/MWh. API2 coal prices are up by 5.50 USD since last week, with the Cal-26 contract trading at 114.50 USD/tonne. Front-year gas prices are down by 1.180 EUR since last week, with the TTF Cal-26 trading at 33.725 EUR/MWh. EUR/USD is up by 140 points since last week and is currently trading at 1.1760.

Price development of EUA Dec2025 futures contract