Pridobite najnovejše informacije iz trga emisijskih kuponov in se prijavite na brezplačno tedensko prejemanje novic

This newsletter was published 3.9.2025 at 17:31pm CEST

The current prices on the European carbon market are as follows:

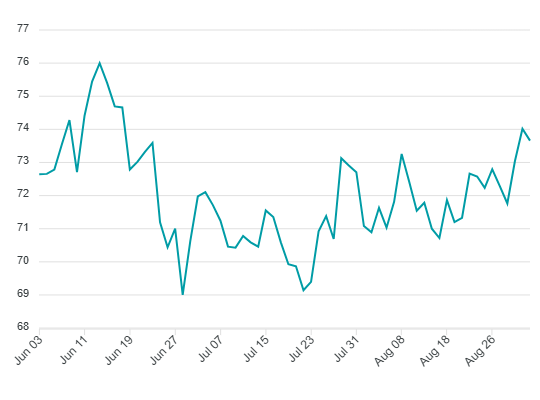

t appears that late compliance buying, along with investment funds accumulating length, created enough pressure to push through a key technical level at 73.35 EUR for December 2025 futures. This level had acted as strong resistance multiple times before. Adding confirmation to the underlying bullish bias are the very strong auction results. Despite slightly lower cover ratios, auctions continue to clear solidly, even when the market is trading at daily highs. Interestingly, the rally has not been fuelled by any specific bullish news. However, many meteorologists are forecasting a colder-than-usual winter, which could increase energy demand. If supply remains tight, that could reinforce bullish tendencies going forward. However, the most recent CoT report raises some questions. It shows that financial players have amassed their largest long position in five months. This begs the question: is this breakout driven by genuine demand or is it simply another cycle of speculative buying and selling, as we have seen repeatedly throughout the year. Other markets in the energy complex are also sending mixed signals. While the correlation between EUAs and TTF gas remains intact, EUAs have shown greater sensitivity to the upside, whereas gas prices have tended to make sharper moves to the downside when markets weaken.

German power prices are up by 1.25 EUR since last week, with the front-year contract trading at 85.95 EUR/MWh. API2 coal prices are down by 1.25 USD since last week, with the Cal-26 contract trading at 103.55 USD/tonne. Front-year gas prices are up by 0.055 EUR since last week, with the TTF Cal-26 trading at 31.950 EUR/MWh. EUR/USD is up by 80 points since last week and is currently trading at 1.1680.

Price development of EUA Dec2025 futures contract

Nazaj