Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 10.11.2021 at 17:08pm CEST

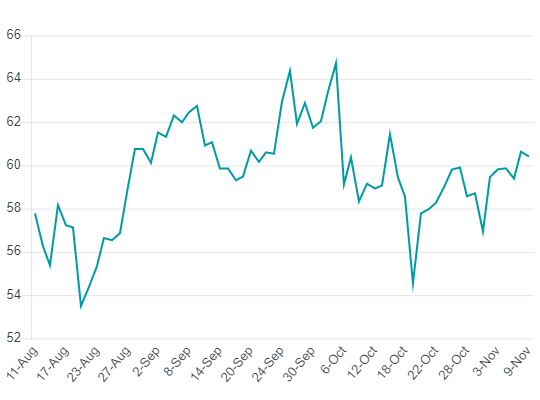

The current prices on the European carbon market are as follows:

After sixteen consecutive daily closes below 60 EUR, EUAs finally managed to close a trading day above the level on Monday. Since then, it has provided strong technical and psychological support, since all dips below have been absorbed so far. It might appear that many options call holders have already locked in some of the yearly profits and are waiting for another push to the upside. For now, the nearest resistance level seems to be near record highs, especially due to established long-term bullish trend. Many are speculating that major move might happen during the winter, however central Europe may not experience colder temperatures just yet. Bearish factor in pricing EUAs could be increased gas imports from Russia via existing pipelines. Long awaited natural gas flows to Europe have increased on Monday, November 8, which has been in line with expectations. Imports have decreased supply tightness, and most important global gas markets fell by around 20 percent in only a few days. Auctions in the past week have been clearing near secondary market prices, but with slight discount. Nearing quarterly option expiry in December, increased gas imports and modest weather could mean that yearly price range has already been established, however one should not be surprised if price continues trending north.

German power prices are down by 5.90 EUR since last week, with the front year contract trading at 110.85 EUR/MWh. API2 coal prices are down by 9.50 USD since last week, with the Cal22 contract trading at 104.00 USD/tonne. EUR/USD is down by 60 points since last week and is currently trading at 1.1515.

Price development of EUA Dec2021 futures contract

Back