Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 27.7.2022 at 16:54pm CEST

The current prices on the European carbon market are as follows:

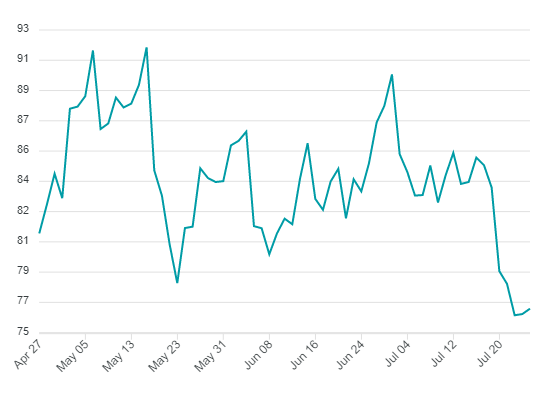

After a week of heavy selling, EUAs might finally be entering a consolidation phase. For the past few days EUAs have been trading between 75 and 80 EUR, down by almost 15 EUR from monthly highs. It seems that market has found equilibrium, since daily trading ranges have narrowed but average trading volumes picked up quite a bit. Dynamics on auctions have shifted a bit as well, since some of them cleared well above secondary market recently. Upcoming halved auctions in August could provide a bullish short-term bias, which might at least support current sideways range. Despite that, EUAs have been an underperformer in comparison to other markets in European energy complex, especially German power and gas. The main reasons might be concerns about inconsistent gas supply, fluctuations of daily nominations and general fear of shortage, which has been very bullish for these two commodities. Quite the opposite has been true for carbon, which has started to be negatively correlated to gas and power again. Upward pressure in gas might help push EUAs below the current range but for now EUA market remains fairly balanced.

German power prices are up by 46.50 EUR since last week, with the front year contract trading at 373.00 EUR/MWh. API2 coal prices are up by 30.00 USD since last week, with the Cal23 contract trading at 290.00 USD/tonne. EUR/USD is down by 80 points since last week and is currently trading 1.0120.

Price development of EUA Dec2022 futures contract