Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 1.5.2024 at 16:13pm CEST

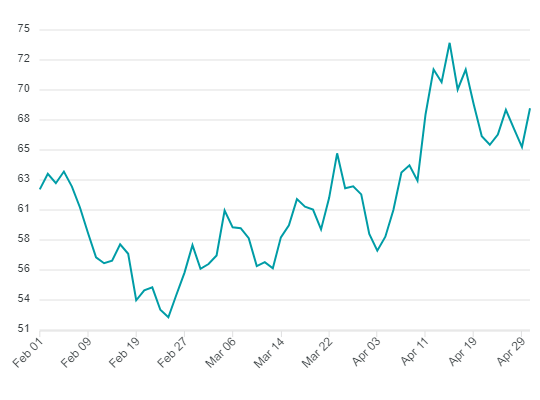

The current prices on the European carbon market are as follows:

Carbon has been range bound for several days already, as energy markets enter a period with balanced supply and demand. Warmer weather and anticipation of higher renewable power generation have been providing some bearish pressure, while short covering provided support for EUAs. Buyers have been accumulating relentlessly around 65 EUR per tonne, however, when the price came close to 70 EUR, the buying pressure subdued. Many auctions in the past week offered some, but not a substantial discount below the secondary market, however, EUAs have been resilient and continued to be positively correlated to gas. According to the weekly CoT report, investment funds continue to decrease the net short exposure, which is currently sitting at just over 18 million tonnes. In relative terms, the funds already covered more than half of the position from late February, which was at the time at a record 39 million tonnes short. It seems that the market has been over time able to absorb the liquidity coming from short covering, and the whole process seemed quite under control. Although the energy complex looks quite unexciting at the moment, an increasing support for gas prices might be coming from Asia. The heatwave caused a spike in liquefied natural gas demand, and consequently, the European gas storages have been filling at a slower pace. The UK emission allowances have been in the meantime quietly trading in an even narrower range before the compliance deadline, at around 36 GBP per UKA. In contrast to EUAs, investment funds have been holding a long net position in UKAs; however, the market was unable to trade above 40 GBP since early January this year.

German power prices are up by 3.26 EUR since last week, with the front year contract trading at 90.51 EUR/MWh. API2 coal prices are down by 6.25 USD since last week, with the Cal-25 contract trading at 109.75USD/tonne. Front year gas prices are up by 0.525 EUR since last week, with the TTF Cal-25 trading at 33.625 EUR/MWh. EUR/USD is down by 10 points since last week and is currently trading 1.0680.

Price development of EUA Dec2024 futures contract