Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 13.8.2025 at 17:27pm CEST

The current prices on the European carbon market are as follows:

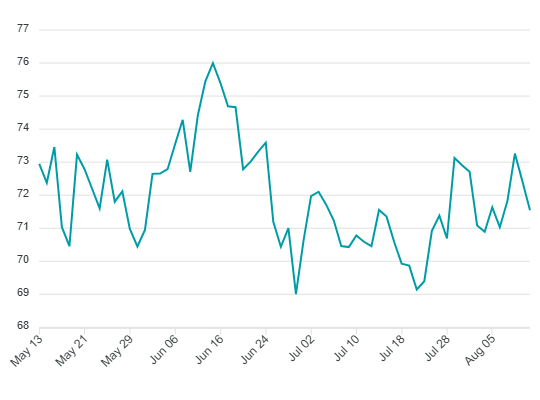

EUA prices ended the week almost unchanged, repeating a familiar pattern where brief rallies are quickly erased, keeping the market locked in its established range. Traders remain focused on the upcoming Putin–Trump meeting, with speculation that sanctions on Russian gas could be eased in exchange for a ceasefire in Ukraine. Falling natural gas prices have improved the competitiveness of gas-fired generation over coal, reducing EUA demand from the power sector. However, Commitment of Traders data shows investment funds increased their net long positions by more than 8 million tonnes last week, and around 14 million tonnes over the past three weeks. Despite this substantial buying, prices have failed to break higher, suggesting that speculative length is being countered easily. August’s options expiry was quiet, with less than 1 million tonnes of nearly 11 million tonnes in open interest ending in the money.

German power prices are down by 0.79 EUR since last week, with the front-year contract trading at 85.70 EUR/MWh. API2 coal prices are down by 4.00 USD since last week, with the Cal-26 contract trading at 107.00 USD/tonne. Front-year gas prices are down by 0.750 EUR since last week, with the TTF Cal-26 trading at 32.600 EUR/MWh. EUR/USD is up by 70 points since last week and is currently trading at 1.1710.

Price development of EUA Dec2025 futures contract

Back