Get the latest carbon markets info and subscribe now to our free weekly carbon newsletter

This newsletter was published 1.7.2026 at 17:20pm CEST

The current prices on the European carbon market are as follows:

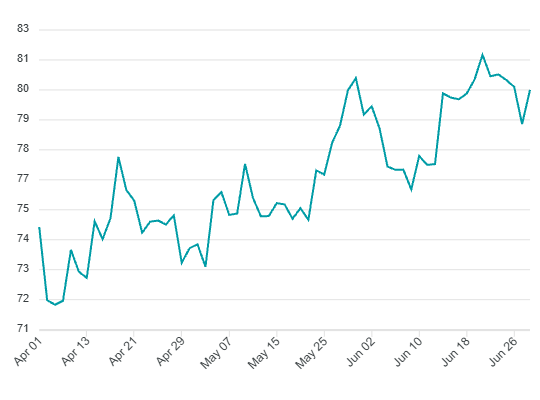

EUA prices weakened over the past week, with the December 2026 futures contract falling back below the €80 level and testing its 200-day moving average. Despite the softer price action, the market remains focused on the European Commission’s upcoming review of the EU Emissions Trading System (EU ETS), due on July 15. Speculative positioning continued to build, with the latest Commitment of Traders (CoT) report showing investment funds increasing their net long position to around 62 million tonnes. While this reflects growing confidence ahead of the ETS review, the larger speculative exposure could also increase the risk of volatility if policy expectations are not met. Political attention centred on a meeting of 12 member states, led by Poland, to coordinate priorities for the upcoming ETS reform. Discussions covered potential changes to the Market Stability Reserve (MSR), expansion of the Modernisation Fund, revisions to free allocation benchmarks, and Poland’s renewed call to delay ETS2 beyond its current 2028 start date. With member states beginning to align their negotiating positions, the Commission’s proposal on July 15 is expected to be the key driver of EUA prices in the coming weeks.

German power prices are unchanged since last week, with the front-year contract trading at 92.50 EUR/MWh. API2 coal prices are similarly only down by 0.60 USD since last week, with the Cal-27 contract trading at 110.60 USD/tonne. Front-year gas prices are up by 0.150 EUR since last week, with the TTF Cal-26 trading at 34.580 EUR/MWh. EUR/USD is up by 60 points since last week and is currently trading at 1.1390.

Price development of EUA Dec2026 futures contract